Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

New Zealand

New Zealand

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

New Zealand

Netherlands

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

The global economy has absorbed the initial shock from the war in Iran better than feared, but the outlook rests on fragile assumptions. The disruption to energy flows through the Strait of Hormuz since the start of the conflict pushed up oil, gas and fertiliser prices just as growth was already slowing down amid trade friction and geopolitical uncertainty. Since the June ceasefire, energy prices have fallen back markedly and inflation expectations remain broadly anchored, reducing the risk of a sustained spiral of higher prices and weaker growth. At the same time, the global economy continues to benefit from the US-led AI and technology investment boom. However, the ceasefire remains fragile and the renewed military strikes between the US and Iran in early July highlight how quickly disruption to energy markets could re-emerge. While our baseline assumes a gradual reopening of the strait and further easing in energy prices, downside risks to the outlook remain elevated.

Global GDP growth is forecast to slow to 2.4% in 2026, from 3.0% in 2025, before recovering to 3.1% in 2027. The impact of the Iran war and the closure of the Strait of Hormuz pushed up energy and fertiliser prices, creating a mild stagflation shock. This is being partially offset by the AI boom, a less severe trade war and continued fiscal support. Under our baseline assumption that the strait continues gradually reopening a sharper downturn is prevented.

Global trade growth is expected to slow after a stronger than expected 2025. Trade grew by 4.6% last year, supported by tariff frontloading and strong demand for AI-related goods, especially from Asia. This momentum is unlikely to be repeated. Higher energy prices, weaker import demand and ongoing trade-policy uncertainty are expected to keep trade growth below 2% in 2026, before it recovers to around 3% in 2027.

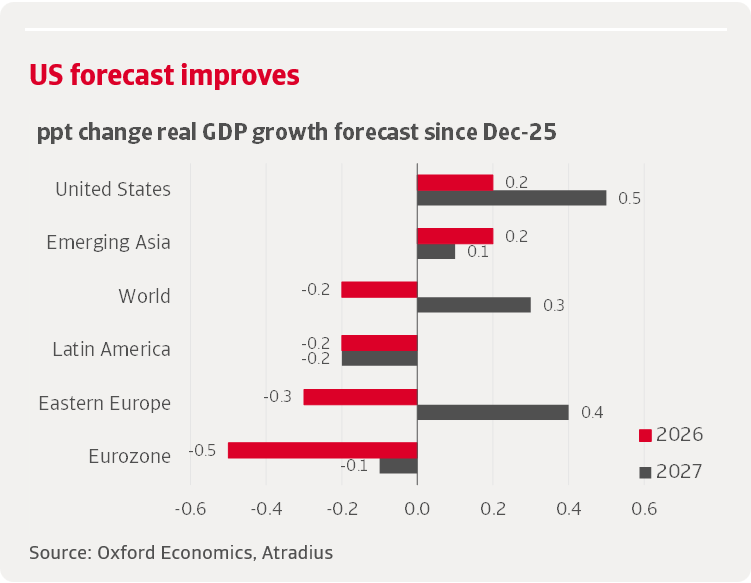

Advanced economies are set for slower and more uneven growth. GDP growth is forecast to ease to 1.5% in 2026, from 1.9% in 2025, before improving to 2.0% in 2027. The US remains the strongest performer, helped by AI investment, fiscal support and domestic energy production, but growth is increasingly concentrated in fewer sectors. The eurozone is more exposed to imported energy and weak manufacturing competitiveness, while the UK and Japan face country-specific fiscal and confidence constraints.

Emerging market economies remain the main source of global growth, but momentum is weaker than usual. EMEs are forecast to grow by 3.7% in 2026 and 4.2% in 2027. China’s growth is expected to slow from 4.8% in 2026 to 4.6% in 2027, as export resilience only partly offsets weak domestic demand. India remains the fastest-growing major economy, despite being the most exposed to energy supply disruptions through the Strait of Hormuz.

A re-escalation of the US-Iran conflict is the main downside risk to the outlook. If fighting resumes and the Strait of Hormuz remains closed until Q4, energy prices would spike again, inflation would rise and global GDP growth would slow to recessionary levels of 1.9% in 2026 and 1.4% in 2027.

For a complete overview of the impacts and risks of the rise in AI, ongoing trade war and more on our global economic outlook, download the full report available in the related documents section below.