Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

New Zealand

New Zealand

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

New Zealand

Netherlands

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

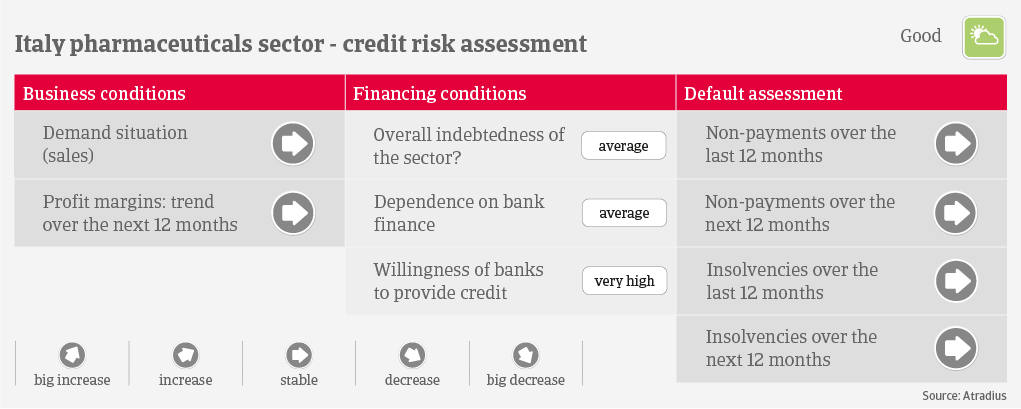

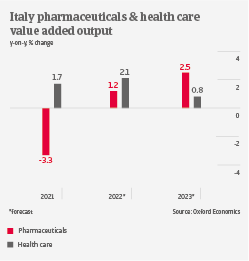

Italy´s pharmaceuticals industry accounts for about 2% of global production, with 85% of production exported. In general, Italian drug producers record high margins, but since H2 of 2021 they are being affected by a sharp increase in energy prices. Margins of wholesalers and distributors are generally tight, due to high transport costs, discounts to customers and outstanding receivables. On top, there is a 3% margin cap for sales of prescription drugs in the Italian market. Pharmacies try to compensate this with sales of supplements and cosmetic products.

In Italy, public healthcare expenditure per capita amounts to EUR 280, 30% less than the EU average. While healthcare spending growth will be rather modest in 2022 and 2023, mid-and long-term demand will be driven by demographic developments. The ageing population in Italy will trigger an increase in medical treatments, in particular for chronic diseases.

In general, pharmaceutical producers are well capitalised and not highly geared. In contrast, capitalisation of wholesalers is often low and coupled with high indebtedness, high working capital requirements and steady investments in warehouses across the country, and related logistics. In this segment days sales outstanding (DSO) and days of inventory outstanding (DIO) are rather high and businesses require bank loans in order to compensate slow payments from their customers. It helps that banks are generally willing to provide loans to all subsectors, including this segment. The main reason is that pharmaceuticals is performing better than other Italian industries, with a history of low default rates. We expect that both non-payment notifications and insolvencies will remain low in 2022.

Our underwriting stance is very open for drug producers, due to low gearing, high margins and strong export performance. We have a prudent approach for wholesalers/distributors, in particular for businesses in cooperatives, as their solvency is dependent on the timely payment of their affiliates (pharmacies). The same accounts for pharmacies, due to strong competition from hospitals and para-pharmacies, which puts pressure on their margins.